Capital Project Guidelines

The Capital Project Guidelines, prepared by the Office of the University Controller and Financial Management, are established to clarify the minimal dollar threshold for Capital Projects and to identify other characteristics of Capital Projects. They are intended for the use of the Office of the University Controller, the financial management staff reporting to the Senior Associate VP of Operations, and the University Budget Office.

Generally Accepted Accounting Principles dictate that capital assets with a useful life exceeding one year be capitalized and depreciated over the expected useful life subject to the application of the theory of materiality. The theory of materiality allows organizations to elect not to capitalize every asset with a useful life of greater than one year based upon the asset’s immaterial impact on the financial statements.

Capital Projects may either be funded with the general funds of the University, through borrowing (either external or internal), or with funds provided by departments. Throughout this document, the term “Project Sponsor” is used to refer to departments that provide funding for capital projects. Project Sponsors include Student Housing, Parking, and academic departments.

- The Guidelines

Capital Projects are those projects:

- With a project budget equal to or in excess of $100,000, net of any equipment tobe purchased. (Equipment is capitalized pursuant to the Furniture and Equipment Capitalization Threshold policy).

- Whose improvement has an estimated useful life of greater than one year and

- Which add new space or

- Change the intended use (functionality) of existing space or

- Extend the useful life of the asset / space or

- Change or replace a significant building system (HVAC, Elevators).

The first factor relates to the materiality threshold and therefore must be met before the remaining factors are considered. Any project meeting the first factor test and one or more of the remaining factors are to be considered Capital Projects and designated with a “PN” funding source.

- Other Characteristics

In order to account for and present projects accurately as assets or plant alterations, the full scope of a project should be documented at the time a proposed project budget is submitted. Combining more than one activity in a project should be avoided for the following reasons:

- Plant alteration cost could be mistakenly capitalized

- Assets may be incorrectly defined and misleading

- The estimated useful life may be inaccurate

Examples

A complete building façade replacement coupled with window replacement = 1 Project

A major roof repair coupled with a new or renovated patio area = 2 projects

ISS cabling project that provides network support to multiple buildings = 1 project

In the first example, the activities are similar in that they both relate to the exterior refurbishment of the building façade.

In the second example, the roof and the patio are mutually exclusive activities. Each activity should be considered separately and the decision to capitalize the roof or the patio should be determined by applying the above guidelines to each of the activities.

In the third example the project supports many facilities and the cost to each facility is not easily identified. The cost of the overall project is allocated to each facility upon completion.

To clarify the construction of a new building is considered one project. Renovation of multiple classrooms in one building at the same time can be considered one project. However, the renovation of the fire protection system throughout a building in phases as renovations to the building occur should be evaluated by applying the above guidelines separately for each phase.

If it is absolutely necessary to combine unrelated projects into one PN project fund, such as those described in example 2, additional details of the scope should be provided in advance of the project to ensure all parties (Facilities/Real Estate, the Project Sponsor, Budget Office and Office of the University Controller) are aware of and acknowledge the multiple facets of the project and agree upon the proper funding code (PN vs. PM) and capitalization treatment. In addition the supporting documentation submitted with the initial budget request should include an estimate of the cost of each project individually.- Plant Maintenance / Alteration Projects

Projects that do not meet the criteria for capital projects are designated as Plant Maintenance/Alteration Projects. A “PM” Funding Source will be used to account for these projects. A minimum estimated cost of $50,000 is necessary to establish a Plant Maintenance/Alteration project. Projects falling below this threshold are accounted for within the operating budget.

- Feasibility Studies

Feasibility studies performed to determine the appropriateness of a construction/renovation project or to assist the University in establishing a scope should be established as a PN project if the project is expected to meet the criteria of a Capital Project above. These costs are to be capitalized as Construction in Progress (CIP) until a decision is reached on whether the University will proceed with the project.

If the University proceeds with the project, the cost of the study will be incorporated into the asset cost. If the University decides to abandon the project the cost of the study will be expensed at that time.

- Timing of Project Request

Capital Projects and Plant Maintenance /Alteration Projects are established in Oracle/EAS by the Office of the University Controller after the Budget Office has submitted the GL Account Maintenance form.

All project requests should be submitted at least thirty days in advance of the start date to the Budget Office. This will provide time to resolve funding issues, set-up the appropriate PN or PM Funding Source in Oracle/EAS, and enter the budget in Oracle/EAS. Project requests can be submitted as soon as the capital budget is approved by the Board of Trustees in May.

If the funding for a project is coming from a Project Sponsor/Department instead of from the capital budget the following steps should be followed:- Project Sponsor will work with their budget analyst to agree on funding

- Project Sponsor will communicate agreed upon funding to the Project Administrator.

- Project Administrator will communicate project details via a Budget Change Request (BCR) to the Budget Office.

Required Budget Change Request (BCR) Documentation – 8 point Memo

- Site - building name and street address

- Scope

- Necessity - for example, change in use, provides additional use, etc.

- Cost Estimate - provide support such as bids received, developing schedules, etc.

- Funding Source

- Schedule - estimated start and occupancy/completion date

- Service Life

Required Budget Change Request Approvals

- Director of Project Management

- Facilities Finance Director

- Associate Vice President for Facilities

- Senior Associate Vice President for Operations

- Project Stages

The budgets for projects over $3 million should be requested in stages.

- Stage 1: Planning and Design – submit detailed account budget for preliminary dollars needed.

- Stage 2: Final for Guaranteed Maximum Price (GMP) – submit detailed account budget for remaining project dollars needed including contingency

The budgets for smaller and Repair, Replacement, and Renewal (RRR) projects should be requested in entirety.

- Changes to the Budget

During the life of a project, the original budget may need to be reevaluated based on unforeseen conditions (e.g., unanticipated replacement/upgrade of infrastructure), changes in estimated costs (e.g., escalating labor costs), or the desire to expand the original scope of the project (e.g., to renovate additional space).

The expansion of project scope is discretionary in that it was not identified as necessary at the time the original project budget was approved.

While the Project Administrator should inform the Budget Office of anticipated variances to the approved project budget, a Budget Change Request to revise the budget should only be submitted if the anticipated additional costs exceed the following threshold, depending on project size:

Original Project Budget Budget Change Threshold

$500,000 or more 10% or more of the approved budget

$499,999 or less No budget change

Budget change requests for changes not meeting the above thresholds are not necessary. However, such changes should be communicated to the Budget Office as soon as they are known so that the corresponding funding changes can be anticipated and reflected in the project report.

In addition to determining whether a project budget should be revised, additional review is necessary before expanding the scope of a project. Even if the expanded scope can be accommodated within the current budget, it represents the discretionary expenditure of University resources that could be used for other purposes. Therefore, if the cost of the additional scope represents 10% or more of a current project budget that is funded by general University funds (including debt), the Project Administrator must request Budget Office approval before proceeding.If the expanded scope is the result of a request from a Project Sponsor and the Project Sponsor is willing to fund any additional costs associated with the additional scope, the Budget Office’s role is limited to confirming the Project Sponsor’s ability to fund the additional scope.

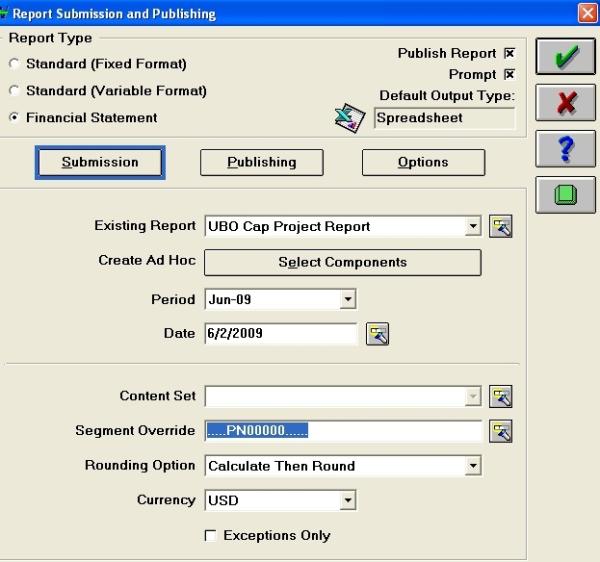

Budget changes that do not meet the threshold for a Budget Change Request will be tracked using a project report that reflects current budget and funding. The report can be run from ADI if the following parameters are used (be sure to put in the applicable project number in the Segment Values field):

Procedures for the development of the project summaries used in the quarterly CIP review will be incorporated into these guidelines at a later date.